Business Energy Broker

Utility SwopShop Weekly Market Insights Week Ending 3rd July

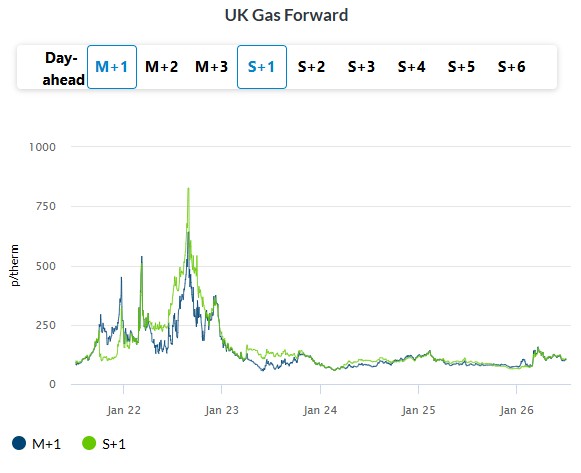

Gas

Ongoing uncertainty over control of the Strait of Hormuz and potential transit fees continued to underpin LNG risk premiums, despite indications of progress in the Doha negotiations and U.S. President Donald Trump playing down the likelihood of conflict. Against this backdrop, British gas prices moved higher on Thursday, with the NBP spot contract climbing 2.2% to 103.95 p/therm. Further along the forward curve, the Winter 2026 contract rose by nearly 2% to settle at 108.80 p/therm.

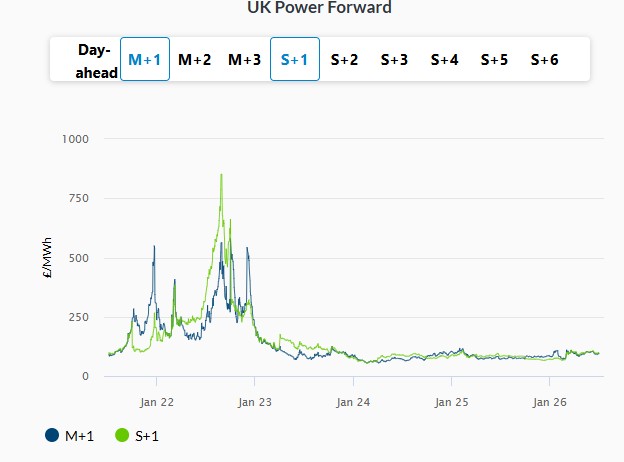

Power

British power prices strengthened on Thursday, with the day-ahead contract jumping nearly 66% to 89.79 GBP/MWh. The sharp increase was fuelled by a significant decline in wind generation, forecast to fall to around 5.4 GW, while the 595 MW outage at Heysham 2-7 lowered nuclear availability from 63% to 54%. Further along the forward curve, the Winter 2026 contract followed gains in the gas market, rising 1.3% to close at 98.21 GBP/MWh.

Disclaimer

The contents of this webpage, such as text, graphics, images, and other material contained on the Utility SwopShop Ltd Site (“Content”) are for informational purposes only and are designed to provide market information based on market information available from energy suppliers in the UK. The Content is not intended to be a substitute for energy market professional advice and does not provide contract pricing for the delivered price of energy but does provide an indicator of the current wholesale commodity elements of the delivered price